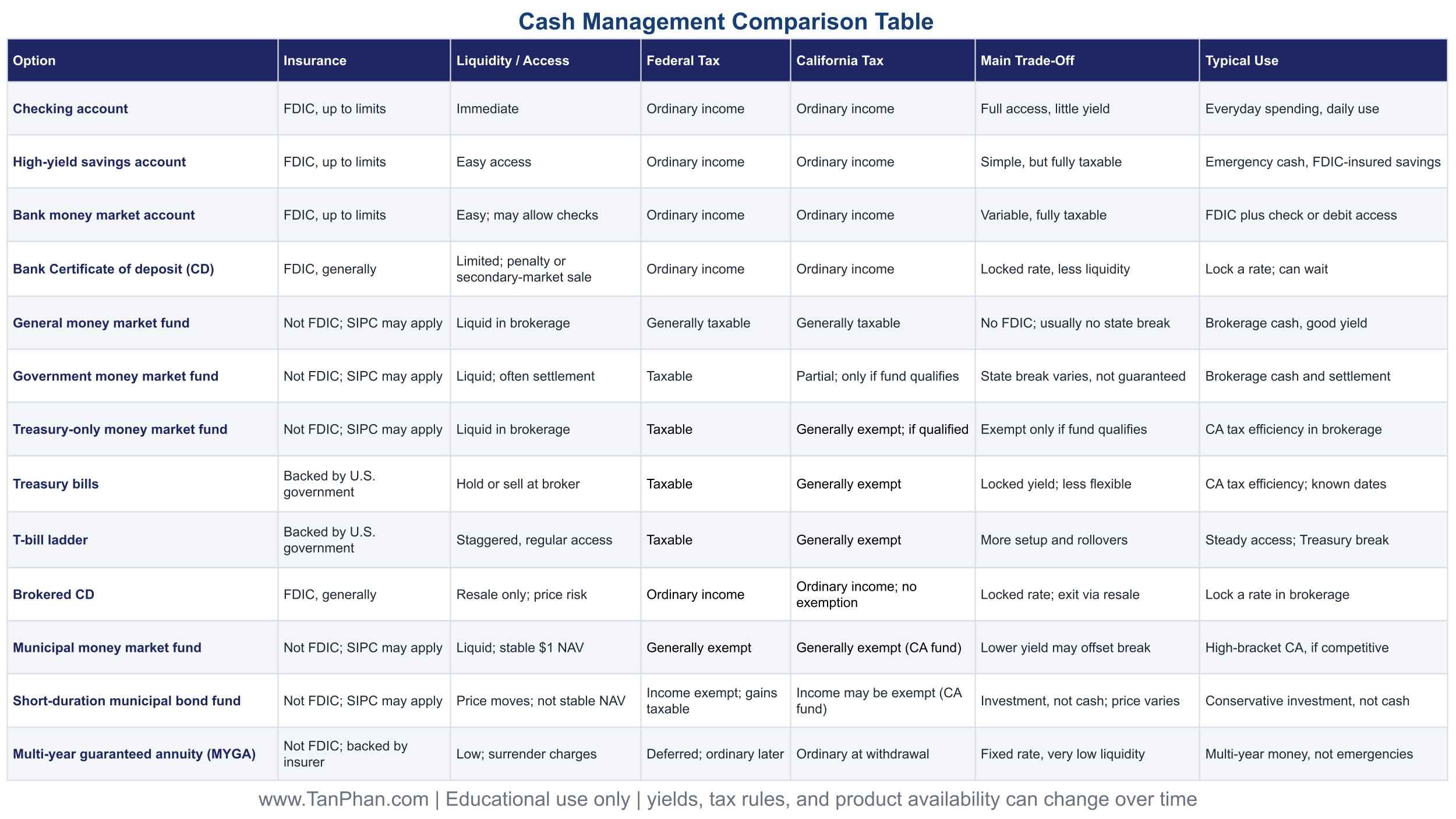

The Mechanics of Cash Management: Liquidity, Tax Treatment, and After-Tax Yield

Hi everyone, my name is Tan, and I am an independent CERTIFIED FINANCIAL PLANNER™ practitioner at TAN Wealth Management. Today’s educational video is on cash management.

What Is the Money For?

The first question we need to ask is, what is the money for? If the money is needed today for bills, spending, or transfers, it belongs in a checking account. A checking account is mainly for liquidity and convenience, not for earning a high interest rate. If we want the money to stay available but also earn more than a checking account, then we can look at other cash management options. This may include a high-yield savings account, a money market fund, a Treasury-only money market fund, Treasury bills, and other cash management tools. The better fit depends on what matters most. That may be FDIC insurance, convenience, keeping the cash inside a brokerage account, getting a competitive yield, or improving the after-tax result.

For states with income tax, we need to perform the tax-equivalent yield calculation to compare the after-tax yields. Two options may show the same stated yield, but the after-tax results can differ. This is why I do not start with the highest yield. I start with what the money is for, and the right account usually falls out of that. We need to know that cash management options are not meant to build long-term wealth like stocks. These are liquidity tools. We want this money safe, available when we need it, and earning something reasonable in the meantime.

High-Yield Savings Accounts and Savings Accounts with competitive rates

A high-yield savings account and savings account is a bank deposit. It is generally FDIC-insured up to $250,000 per depositor, per insured bank, per ownership category. Interest from a high-yield savings account and a savings account is taxed as ordinary income. In most cases, that means it is taxable at both the federal and California levels. A high-yield savings account and a savings account works well if our top concerns are FDIC insurance, simplicity, and easy access to the cash. It may be less attractive for a high-income California resident holding a large cash balance in a taxable account, because the after-tax return may be lower than other options.

Bank Money Market Accounts

A bank money market account is also a bank deposit, so it is generally FDIC-insured up to applicable limits. It may offer features like check-writing or debit card access, and the rate is usually variable. From a tax standpoint, the interest is generally taxed as ordinary income at both the federal and California level. A bank money market account is worth considering if we want FDIC insurance, easy access, and other features like check-writing or access to a debit card.

Money Market Funds

A money market fund is a mutual fund that invests in short-term securities. It is not a bank deposit, and it is not FDIC-insured. If the fund is held inside a brokerage account, SIPC coverage may apply, but SIPC mainly protects against brokerage firm failure. It does not protect against investment losses or market fluctuations. The tax treatment depends on what the fund owns. Some money market funds generate income that is fully taxable. Treasury-only money market funds may be more tax-efficient for investors who live in states with income tax, such as California. That is because income from U.S. Treasury obligations is generally exempt from state income tax. A money market fund makes sense if we are keeping cash inside a brokerage account, we want a competitive yield, and we want that cash ready for investing, rebalancing, or accomplish other objectives.

A high-yield savings account, a bank money market account, and a brokerage money market fund may all be used for cash, but the insurance, tax treatment, and use case can be very different.

“Key takeaways

- Both high-yield savings accounts and money market funds provide safe and accessible places to park your cash, but they come with a few key differences.

- High-yield savings accounts are FDIC-insured up to $250,000 per account holder, while money market funds are not, though they’re still considered low-risk investments. [Money market funds are not FDIC-insured. They may have

SIPC insurance up to $500,000, but this coverage is only against brokerage failure, not against investment losses or market fluctuations.]

- Money market funds and high-yield savings accounts often respond quickly to Federal Reserve rate changes so the yield you earn can change over time.

- Both options are ideal for short-term savings but won’t generate significant long-term wealth or outpace like stocks or retirement accounts.”

https://www.bankrate.com/investing/hysa-vs-money-market-fund

“How is interest from a high-yield savings account taxed? Interest on a high-yield savings account — like interest from certificates of deposit (CDs) or money market accounts — is usually taxed at your ordinary income rate for the year it’s earned. You normally pay federal and state taxes on interest earned from a HYSA.”

https://www.wsj.com/buyside/personal-finance/taxes/do-i-get-taxed-on-a-high-yield-savings-account

“Interest on a high-yield savings account is taxable. It’s taxed the same as your regular earnings on your federal tax return.”

https://www.experian.com/blogs/ask-experian/are-high-yield-savings-accounts-taxed

“The interest you earn in a money market account is taxable as regular income.”

https://www.experian.com/blogs/ask-experian/do-you-pay-taxes-on-money-market-account

“Money market accounts are variable-rate savings products…If the money market is held in a taxable account, the interest earned is taxed as ordinary income.”

https://www.kiplinger.com/retirement/hot-rate-on-a-money-market-account-think-again

Certificates of Deposit

A certificate of deposit, or CD, can make sense when we are willing to give up some liquidity in exchange for a locked interest rate. Bank CDs generally have FDIC insurance, but they may charge an early withdrawal penalty if we need the money before maturity.

Brokered CDs are different. They are purchased inside a brokerage account and may also have FDIC insurance, but they usually do not have a simple early withdrawal option. If we need the money before maturity, we may need to sell the CD on the secondary market. The value could be higher or lower than what we originally paid.

For state income tax residents, taxes matter. CD interest is generally taxable at both the federal and California level. There is no state tax exemption because a CD is a bank obligation, not a U.S. Treasury obligation. This can make a lower-yielding Treasury more attractive after taxes.

For example, assume a one-year CD pays 4.00% and a Treasury security with a similar maturity pays 3.70%. At first glance, the CD appears to be the better option. However, for someone in the 24% federal tax bracket and the 9.3% California tax bracket, the after-tax yields would be:

CD after-tax yield: 4.00% × (1 − 24% − 9.3%) = approximately 2.67%

Treasury after-tax yield: 3.70% × (1 − 24%) = approximately 2.81%

In this example, the CD offers a higher yield before taxes, but the Treasury provides a higher yield after taxes because Treasury interest is exempt from California state income tax.

Money Market Funds

A money market fund is a mutual fund that invests in short-term, high-quality debt such as Treasury bills, government agency securities, repurchase agreements, certificates of deposit, and other short-term securities. Money market funds are commonly used inside brokerage accounts as settlement funds.

Money market funds can be useful for:

• Parking cash temporarily

• Holding emergency reserves

• Keeping cash available inside a brokerage account

• Waiting to invest or rebalance

• Reducing risk during volatile markets

Most money market funds aim to maintain a stable net asset value of $1.00 per share. The share price is designed to stay stable, but the yield can change as interest rates change. Remember that a money market fund is not a bank deposit. It is not FDIC-insured. If it is held inside a brokerage account, SIPC coverage may apply, but SIPC does not protect against investment losses or changes in market value.

What the 7-Day Yield Means

• When comparing money market funds, we look at the 7-day yield. This gives us an estimate of the fund’s annualized yield based on recent income. It is not guaranteed, but it is a useful way to compare one money market fund against another.

• “7-Day Yield: The average income return over the previous seven days, assuming the rate stays the same for one year. It is the Fund’s total income net of expenses, divided by the total number of outstanding shares and includes any applicable waiver or reimbursement. The 7-Day SEC Yield Without Reductions is the yield without applicable waivers or reimbursements.”

https://institutional.fidelity.com/app/proxy/content?literatureURL=%2F9903527.PDF

• The standard 7-day yield includes any fee waivers or reimbursements currently being applied to the fund. Those waivers can increase the yield being shown. The 7-Day SEC Yield Without Reductions removes that benefit and shows what the yield would be without any fee waivers or reimbursements. With reductions means Fidelity is waiving some fees or reimbursing expenses, which can make the reported yield higher. Without reductions means the yield is shown without that support.

• For example, if a fund’s yield would normally be 3.20%, but Fidelity is waiving some expenses, the quoted 7-day yield might show 3.30% instead.

• In that case:

7-day yield: 3.30%

7-day yield without reductions: 3.20%

• The “without reductions” number helps show whether the current yield is being supported by temporary fee waivers or reimbursements.

• “The Standardized 7-Day Current Yield is the average income return over the previous seven days. It is the Fund’s total income net of expenses, divided by the total number of outstanding shares. The yield may differ slightly from the actual distribution rate of a given portfolio because of the exclusion of distributed capital gains or losses which are non-recurring. The SEC Yield is a required yield to quote to clients. This yield does not allow for the inclusion of capital gains or losses.”

https://www.gsam.com/content/dam/gsam/pdfs/us/en/miscellaneous/GLM/money-market-yield-return-defs.pdf

The 7-day yield is the average income return over the previous seven days, annualized. It gives us a snapshot of what the fund is currently yielding if the recent rate were to continue for a full year. It is useful for comparing one money market fund to another, but it is still only a snapshot. It can change. It is not a guaranteed annual return. Some fund companies also show a 7-day yield without reductions, which removes the effect of fee waivers or reimbursements. That can be helpful if we want to see whether the current quoted yield is being supported by temporary fee waivers.

There are a few other terms that can help when comparing money market funds. Weighted Average Maturity, or WAM, is the weighted average maturity of the securities in the fund. Weighted Average Life, or WAL, is the weighted average of the final maturities of those securities. These numbers help describe how short-term the portfolio is and how the fund is positioned. They are not usually the first thing most investors need to focus on, but they can still be useful when comparing funds side by side.

• “Weighted Average Maturity (WAM)

The money market fund’s weighted average maturity (WAM) is an average of the effective maturities of all securities held in the portfolio, weighted by each security’s percentage of net assets. This must not exceed 60 days if the fund is rated.”

https://www.gsam.com/content/dam/gsam/pdfs/us/en/miscellaneous/GLM/money-market-yield-return-defs.pdf

• “Weighted Average Life (WAL)

The money market fund’s weighted average life (WAL) is an average of the final maturities of all securities held in the portfolio, weighted by each security’s percentage of net assets. This must not exceed 120 days by SEC Rule 2a-7.”

https://www.gsam.com/content/dam/gsam/pdfs/us/en/miscellaneous/GLM/money-market-yield-return-defs.pdf

Example of a difference in yield:

If Fund A 7 day SEC yield is 4.19%

If Fund B 7 day SEC yield is 4.17%

If we invest $100,000 in a fund with a difference in yield of 0.02%

Convert the difference in yield to a decimal: 0.02% = 0.0002

Investment Amount × Difference in Yield = Cost

$100,000 × 0.0002 = $20

Annual cost = $20

This is the amount we give up per year on a $100,000 investment when the yield difference is 0.02%.

• Fidelity® Government Money Market Fund (SPAXX)

Minimum to Invest $0.00

7-Day Yield, AS OF 03/10/2026, +3.30%

https://fundresearch.fidelity.com/mutual-funds/summary/31617H102

If we invest $100,000 × 3.30% = $3,300 is the estimated annual income.

• Fidelity® Government Money Market Fund Premium Class (FZCXX)

Minimum to Invest $100,000.00

7-Day Yield, AS OF 03/10/2026, +3.40%

https://fundresearch.fidelity.com/mutual-funds/summary/31617H706

If we invest $100,000 × 3.40% = $3,400 is the estimated annual income.

• On a $100,000 investment, SPAXX at a 3.30% 7-day yield would generate about $3,300 per year, while FZCXX at a 3.40% 7-day yield would generate about $3,400 per year. Based on the yields as of March 10, 2026, FZCXX is yielding about $100 more per year than SPAXX. Please keep in mind that the 7-day yield can change, so this is only a current snapshot and not a guaranteed annual return. Fidelity lists these as the funds’ current yields as of that date. The same strategy can be sold in multiple share classes with different expense ratios, and the difference flows straight into the yield.

Why Money Market Fund Holdings Matter

Money market funds do not all hold the same securities, and for California investors that difference is worth paying attention to. Two funds may both be called money market funds, or even government money market funds, but the underlying holdings can be very different. One fund may hold mostly direct U.S. Treasury securities, while another may hold a mix of Treasuries, agency debt, repurchase agreements, and other short-term instruments. That difference shows up at tax time, so the fund name by itself does not tell us much. A government money market fund and a treasury-only money market fund can sit right next to each other and still leave us with different after-tax results. What we actually want to know is what the fund holds, and how much of its income is exempt from state income tax.

The holdings usually fall into a few categories:

• U.S. Treasuries. Treasury bills, notes, and bonds are debt obligations issued by the U.S. government and backed by the full faith and credit of the U.S. government. On credit risk, these are generally seen as the safest in this category. U.S. Treasury securities, including Treasury Notes and Treasury Bonds, are debt obligations issued by the U.S. government to finance its operations.

• Agency debt. This is debt issued by government-sponsored enterprises or government-related agencies, such as Fannie Mae, Freddie Mac, and Ginnie Mae. These entities help provide liquidity, stability, and affordability to the mortgage market, but their debt is not the same as a direct U.S. Treasury obligation. Fannie Mae and Freddie Mac are privately owned government-sponsored enterprises with an implicit expectation of government support. Ginnie Mae, on the other hand, is government-owned and explicitly backed by the U.S. government. This matters because not everything that sounds government-related is taxed or backed the same way.

- “The term "government-sponsored enterprise" means a corporate entity created by a law of the United States that- (A)(i) has a Federal charter authorized by law; (ii) is privately owned, as evidenced by capital stock owned by private entities or individuals; (iii) is under the direction of a board of directors, a majority of which is elected by private owners; (iv) is a financial institution with power to- (I) make loans or loan guarantees for limited purposes such as to provide credit for specific borrowers or one sector; and (II) raise funds by borrowing (which does not carry the full faith and credit of the Federal Government) or to guarantee the debt of others in unlimited amounts; and (B)(i) does not exercise powers that are reserved to the Government as sovereign (such as the power to tax or to regulate interstate commerce); (ii) does not have the power to commit the Government financially (but it may be a recipient of a loan guarantee commitment made by the Government); and (iii) has employees whose salaries and expenses are paid by the enterprise and are not Federal employees subject to title 5.”

https://uscode.house.gov/view.xhtml?req=(title:2%20section:622%20edition:prelim)

• What is a Government-Sponsored Enterprise (GSE)?

- “A government-sponsored enterprise (GSE) is a quasi-governmental entity established to enhance the flow of credit to specific sectors of the U.S. economy.

- GSEs do not lend money to the public directly; instead, they guarantee third-party loans and purchase loans from lenders, ensuring liquidity.

- GSEs also issue short- and long-term bonds (agency bonds) that carry the implicit backing of the U.S. government.

- Fannie Mae and Freddie Mac are examples of government-sponsored enterprises.”

https://www.investopedia.com/terms/g/gse.asp

• Repurchase agreements, often called repos. These are short-term transactions that money market funds use to help manage liquidity and earn interest with relatively low risk. A repo is basically a short-term loan backed by securities. One party sells securities and agrees to buy them back shortly after, often the next day, at a slightly higher price. That small difference is the interest earned. Repos are common in money market funds because they help the fund stay liquid and still generate income. But for state tax purposes, repos are usually not treated the same as owning Treasury bills, notes, or bonds directly. Even if the repo is backed by Treasury securities, the income may not qualify as direct Treasury interest.

Taxation of Treasury Funds

July 9, 2025 (phone conversation and email with Vanguard Financial Advisor Services). Below is the response from the Vanguard product specialist.

“We can’t speak directly to a client’s tax filing considerations. That said, the advisor/client should review the U.S. government obligations document in our tax center (attached).

Per the document: A state or local tax office or a tax advisor can help determine whether your state allows the exclusion of some of or all the income earned from mutual funds that invest in U.S. government obligations. If your state allows an exclusion, refer to the next page for the percentage of ordinary dividends derived from U.S. government obligations that may be excluded for each fund that was invested in. To determine the portion of dividends that may be exempt from state income tax, multiply the amount of “ordinary dividends” reported in Box 1a of Form 1099-DIV by the percentage listed in the following table.”

You can call Personal investors at 877-662-7447, Monday through Friday, 8 a.m. to 8 p.m., Eastern time

https://corporate.vanguard.com/content/corporatesite/us/en/corp/contact-us.html

“A state or local tax office or a tax advisor can help determine whether your state allows the exclusion of some of or all the income earned from mutual funds that invest in U.S. government obligations. If your state allows an exclusion, refer to the next page for the percentage of ordinary dividends derived from U.S. government obligations that may be excluded for each fund that was invested in.”

https://investor.vanguard.com/content/dam/retail/publicsite/en/documents/taxes/USGO_012025.pdf

I spoke to a representative at Vanguard and he also emailed me this. “Hello Tan, For a mutual fund/ETF to be exempt from state taxes in California, New York, and Connecticut, at least 50% of the fund’s holdings need to be in Treasuries. This is the case for VUSXX. You can reference the legend on the bottom of each page of the PDF you sent me that says “*This fund meets the threshold requirements for California, Connecticut, and New York, which require that 50% of the fund’s assets at each quarter-end within the tax year consist of U.S. government obligations.” Any fund with a * next to it from that PDF meets that threshold.”

https://investor.vanguard.com/content/dam/retail/publicsite/en/documents/taxes/USGO_012025.pdf

This is where Treasury-only funds come into the conversation, such as Vanguard Treasury Money Market Fund (VUSXX) or Fidelity Treasury Only Money Market Fund (FDLXX). Based on the Vanguard U.S. government obligations income information for 2025, VUSXX had 100.00% of ordinary dividends derived from U.S. government obligations for the period referenced. For a California investor, that 100% figure is the whole point. It is what makes the state tax efficiency real. Vanguard’s materials also note that state rules matter and that a tax advisor or state tax office can help determine whether some or all of the income may be excluded from state income tax.

Why Treasury-Only Funds Matter for California Investors

If we are California investors holding short-term cash in a taxable account, Treasury-only money market funds are usually where we would start. California generally does not tax interest income from U.S. Treasury securities. Because of that, a fund that mainly holds direct Treasuries may be more tax-efficient than a general government money market fund that also holds agency debt and repos. Two funds can show almost the same yield, but the after-tax result for a California investor may be different.

A practical example is VUSXX versus VMFXX. VUSXX is Vanguard Treasury Money Market Fund. VMFXX is Vanguard Federal Money Market Fund, which is often used as a settlement fund. VUSXX might offer a slightly higher yield and potential state tax exemptions. I say “might” because the yield changes. The rate on VUSXX can be higher, lower, or the same as the rate on VMFXX. VMFXX, by comparison, may still be useful and convenient, especially for settlement and check-writing purposes in certain non-retirement accounts, but it does not have the same treasury-only profile. That means a California investor in a taxable account may prefer VUSXX if state tax efficiency is a goal.

U.S. government obligations income information - Vanguard

https://investor.vanguard.com/content/dam/retail/publicsite/en/documents/taxes/usgo-2025.pdf

2025 Percentage of Income from U.S. Government Securities - Fidelity

https://www.fidelity.com/bin-public/060_www_fidelity_com/documents/taxes/ty25-gse-supplemental-letter.pdf

We need these documents because they show how much of the fund's ordinary dividends can qualify for a state income tax exclusion.

Meeting the threshold may make a portion of the income exempt. Falling below the threshold may make the entire distribution taxable. For California, the exemption is effectively all-or-nothing at each quarter-end. The fund needs to meet the threshold at each quarter-end, and all four quarters must pass the test.

Treasury-Only Funds vs. General Government Money Market Funds

A treasury-only money market fund is designed to invest primarily or entirely in direct U.S. Treasury obligations. A general government money market fund is still conservative, and there is nothing wrong with holding one. It just tends to also hold agency securities and repos. For California investors in taxable accounts, that can make a difference. We should not assume two money market funds are interchangeable just because both are low risk and both are government-related. We need to look at the holdings.

How to Calculate the California Exclusion

Money market fund income is usually reported on Form 1099-DIV as ordinary dividends. The form does not always clearly separate how much of the income may be exempt from California state income tax. To figure that out, we generally need to look at the fund company’s year-end tax information. The fund company will usually publish the percentage of income that came from U.S. government obligations. Then we multiply our dividend income from that fund by the published percentage. The result is the amount that may be subtracted from California taxable income on Schedule CA, which is the California tax form used to make adjustments between federal and California taxable income.

2025 Instructions for Schedule CA (540) California Adjustments – Residents

https://www.ftb.ca.gov/forms/2025/2025-540-ca-instructions.html

https://www.ftb.ca.gov/forms/index.html

For example, assume a client earned $1,000 of dividends from VMFXX in 2025, and 66.61% of the fund’s income qualified as U.S. government obligation income. $1,000 x 66.61% = $666.10. That means approximately $666.10 may be excluded from California income. At a 9.3% California marginal tax rate, that is about $62 of state tax savings per $1,000 of dividends. If the client held VUSXX and 100% qualified, the full $1,000 may be excluded, saving about $93. If the client held SPAXX and none of the income qualified for the California exclusion, there would be no California tax savings from this exclusion. This is why the fund’s underlying holdings matter. Two money market funds can have similar stated yields, but very different after-tax results for a California taxpayer.

Tax-Equivalent Yield

Tax-equivalent yield is a way of translating a tax-advantaged yield into the taxable yield another investment would need to offer in order to match it. It is a useful way to compare a treasury-only fund against a fully taxable alternative. If one investment has a tax benefit, what taxable yield would another investment need to offer to match it?

For example, Fund A is exempt from California state income tax. To calculate the tax-equivalent yield of Fund A when the 7-day SEC yield is 4.22%:

• At 5% California tax rate

If the After-Tax Yield is 4.22% and the state tax rate is 5%

Tax-Equivalent Yield = Tax-Free Yield / (1 - Tax Rate)

Pre-Tax Yield = After-Tax Yield / (1 - Tax Rate)

Pre-Tax Yield = 4.22% / (1 - 5%)

Pre-Tax Yield = 4.22% / (1 - 0.05)

Pre-Tax Yield = 4.22% / 0.95

Pre-Tax Yield ≈ 4.44%

• At 7% California tax rate

Tax-Equivalent Yield = 4.22% / (1 − 0.07) → 4.22% / 0.93 ≈ 4.53%

• At 9% California tax rate

Tax-Equivalent Yield = 4.22% / (1 − 0.09) → 4.22% / 0.91 ≈ 4.63%

Why After-Tax Yield Matters More Than Headline Yield

The quoted yield is not the only number we should look at. What matters is what we actually keep after federal and California taxes. A Treasury-only money market fund may show a yield that looks similar to another money market fund, or even slightly lower. But if part or all of that income is exempt from California state income tax, the after-tax result may be better. This is where tax-equivalent yield comes in. It helps us compare a tax-advantaged investment against a fully taxable one. For example, if a Treasury-only fund has a 7-day yield of 4.22% and that income is exempt from California state income tax, the equivalent taxable yield would be higher once we adjust for the state tax savings. The exact number depends on the investor’s tax rate, but the main point is the same. The fund with the highest quoted yield is not always the fund we keep the most from after tax.

Treasury Bills and T-Bill Ladders

Treasury bills can be a strong cash management option, especially for California residents. The main benefit is tax treatment. Interest from Treasury bills is generally exempt from California state income tax. Unlike a treasury-only money market fund, there is no fund percentage to look up and no need to check how much of the fund qualified. You own the Treasury bill directly.

Treasury bills are short-term U.S. government obligations. They are commonly issued with maturities such as “4, 6, 8, 13, 17, 26, and 52 weeks”. Unlike a money market fund, a Treasury bill locks in the yield when you buy it and hold it to maturity. That can be good or bad depending on where interest rates go. If rates fall, you keep the yield you locked in. If rates rise, the Treasury bill does not adjust upward the way a money market fund might.

https://www.treasurydirect.gov/marketable-securities/treasury-bills

One way to manage liquidity is to build a T-bill ladder. For example, instead of putting $300,000 into one Treasury bill, we could split it into three $100,000 purchases of 13-week Treasury bills, spaced one month apart. After the ladder is built, one Treasury bill matures about every month. Each maturity gives us a decision point: use the cash or roll it into a new Treasury bill. Many brokerage firms allow automatic rollover, which can make the process easier.

One important platform difference is TreasuryDirect versus a brokerage account. Treasury bills bought through TreasuryDirect generally cannot be sold before maturity without first transferring them to a brokerage account, and that transfer can take time. If the cash may be needed on short notice, buying Treasury bills inside a brokerage account may be more practical because they can usually be sold on the secondary market before maturity. The trade-off is that selling before maturity may result in a gain or loss depending on market rates at the time.

“Selling a Treasury Marketable Security. You can hold a Treasury marketable security until it matures or sell it before it matures. To sell a Treasury marketable security, you must work through a bank, broker, or dealer. Your first step depends on where your security is held.” Watch out for other rules and the rules might change in the future.

https://www.treasurydirect.gov/marketable-securities/selling-marketable-securities

Municipal Money Market Fund

A municipal money market fund invests in short-term municipal securities issued by states, cities, counties, and other local government agencies. The main benefit is the tax treatment. The income is generally exempt from federal income tax. If it is a California municipal money market fund and the investor is a California resident, the income may also be exempt from California state income tax. This can be useful for higher-income California investors, but only if the after-tax yield is competitive. The tax benefit alone is not enough. We still need to compare a municipal money market fund against other cash options, such as a Treasury-only money market fund or Treasury bills. A municipal money market fund can work for conservative cash needs, such as emergency reserves, tax reserves, near-term spending, or money waiting to be invested. The goal is to stay liquid, keep the principal steady, and provide income that may be exempt from federal and state income tax.

Short-duration municipal bond fund. It is also important not to confuse a municipal money market fund with a short-duration municipal bond fund. A municipal money market fund is designed to maintain a stable $1.00 share price. A short-duration municipal bond fund can move up or down based on interest rates, credit conditions, and market demand. We can view a municipal money market fund as a cash management tool, while a short-duration municipal bond fund is a more conservative investment option.

Examples of municipal money market funds:

• Vanguard California Municipal Money Market Fund (VCTXX)

7 day SEC yield 1.49% as of 05/26/2026

“SEC yield: A non-money market fund’s SEC yield is based on a formula developed by the SEC. The method calculates a fund’s hypothetical annualized income as a percentage of its assets. A security’s income, for the purposes of this calculation, is based on the current market yield to maturity (for bonds) or projected dividend yield (for stocks) of the fund’s holdings over a trailing 30-day period. This hypothetical income will differ (at times, significantly) from the fund’s actual experience. As a result, income distributions from the fund may be higher or lower than implied by the SEC yield. The SEC yield for a money market fund is calculated by annualizing its daily income distributions for the previous 7 days.”

https://investor.vanguard.com/investment-products/mutual-funds/profile/vctxx

• Fidelity California Municipal Money Market Fund (FABXX)

FABXX minimum to invest is $0.0 while FSBXX minimum to invest $1,000,000 as of May 28, 2026.

7 day SEC yield 1.34% as of 05/27/2026

Fund objective - “seeks as high a level of current income, exempt from federal income tax and California state personal income tax, as is consistent with preservation of capital.”

https://fundresearch.fidelity.com/mutual-funds/summary/31606Y306

If the After-Tax Yield is 1.4%, the federal tax rate is 24%, and the state tax rate is 9.3%.

Tax-Equivalent Yield = Tax-Free Yield / (1 - Tax Rate)

Pre-Tax Yield = After-Tax Yield / (1 - Tax Rate)

Pre-Tax Yield = 1.4% / (1 - (24% + 9.3%))

Pre-Tax Yield = 1.4% / (1 - 33.3%)

Pre-Tax Yield = 1.4% / (1 - 0.333)

Pre-Tax Yield = 0.014 / 0.667

Pre-Tax Yield ≈ 0.0210 → 2.10%

If the after-tax yield is 1.4%, and the combined federal and state tax rate is 33.3%, the equivalent pre-tax yield is approximately 2.10%. This means a taxable investment would need to earn about 2.10% before taxes to yield the same 1.4% after taxes. The key takeaway is that a double tax exemption sounds attractive, but it does not automatically make the municipal money market fund the better choice. We still need to compare the current yield, the investor’s tax bracket, the after-tax result, and the risks each fund holds at the time of the decision.

Multi-Year Guaranteed Annuities

A multi-year guaranteed annuity, or MYGA, is an insurance contract that pays a fixed interest rate for a set period of time. It is sometimes compared to a CD, but it is not the same thing. The tax treatment is different from a bank account, CD, or money market fund. Interest in a non-qualified annuity grows tax-deferred, so we generally do not pay taxes each year while the money remains in the contract. When money is withdrawn, the gain is taxed as ordinary income at both the federal and California levels. There is no California state tax exemption.

For example, if an insurance company offers 4.95% for 2 years, that usually means 4.95% per year, not 4.95% total over two years. It is still important to confirm the contract details, including whether the interest is compound or simple interest. If 4.95% is the pre-tax rate, what is the after-tax rate if the federal tax rate is 24% and the California tax rate is 9.3%?

After-Tax Yield = Pre-Tax Yield × (1 - Tax Rate)

After-Tax Yield = 4.95% × (1 - (24% + 9.3%))

After-Tax Yield = 4.95% × (1 - 33.3%)

After-Tax Yield = .0495 × (1 - 0.333)

After-Tax Yield = .0495 × 0.667

After-Tax Yield ≈ 0.0330 → 3.30%

The biggest issue with a MYGA is liquidity. If you need the money before the surrender period ends, surrender charges may apply. Some contracts may also include a market value adjustment. If withdrawals are taken before age 59 1/2, gains may also be subject to federal and California penalties, in addition to ordinary income tax.

A MYGA is not FDIC-insured. It is backed by the insurance company's claims-paying ability, so the insurer's financial strength matters. MYGA is not appropriate for emergency cash. It may be appropriate for money with a known multi-year timeline that we do not expect to touch. When comparing MYGA to other cash management tools, we have to factor in taxes, liquidity, surrender charges, penalties, and the insurance company's financial strength.

A MYGA can also be replaced through a 1035 exchange if the owner wants to move from one annuity contract to another. When done properly as a direct exchange, the gain can continue to be tax-deferred. If the owner surrenders the annuity, receives the money, and then buys another annuity, that may create a taxable event.

• “Section 1035(a)(3) provides that no gain or loss is recognized on the exchange of an annuity contract for another annuity contract.”

https://www.irs.gov/pub/irs-drop/rr-07-24.pdf

• “If a Taxpayer receives a check from a life insurance company under a nonqualified annuity contract, the endorsement of the check to a second company as consideration for a second annuity contract does not qualify as a tax-free exchange under § 1035(a)(3). Instead, the amount received is taxable to the extent set forth in § 72(e).”

https://www.irs.gov/pub/irs-drop/rr-07-24.pdf

Why Platform Matters

The best fund in the marketplace may not be the best for us because it depends on the platform we use. Some Vanguard funds may not be available at Fidelity, and some Fidelity funds may not be available at Vanguard. So even if one fund looks better on paper, it may not be practical if our custodian does not offer it. An example of this is Vanguard Treasury Money Market Fund (VUSXX). A Vanguard client may have access to VUSXX, while a Fidelity client may need to use Fidelity’s in-house option, such as FDLXX. Availability can change, and it depends on account type, so it is always worth checking the account before making an informed decision.

Settlement mechanics also matter. At Vanguard, VMFXX is commonly used as the settlement fund, while VUSXX is held as a separate position. If we need cash from VUSXX, we may need to sell it first and wait for the money to settle. At Fidelity, SPAXX is commonly used as the core position. Some Fidelity money market funds may function more like a “pseudo-core” position, where the platform may automatically liquidate the fund to cover trades or debits. This should be confirmed with Fidelity before relying on it, because availability and rules can change at any time.

Yield and taxes are important, but they are not the whole picture. We also need to consider what the platform offers, how quickly we can access the cash, and whether the fund fits how we use the account.

When I contacted Fidelity in fall 2025, the representative told me that VUSXX (Vanguard Treasury Money Market Fund) could not be directly purchased through Fidelity Investments. That may change over time and may also depend on the type of investor, account type, or assets held at the firm. In some cases, it may still be worth checking directly in the account to see whether the fund is available for purchase. I also spoke with my institutional contact at Fidelity, who mentioned that a similar option to VUSXX is Fidelity Treasury Only Money Market Fund (FDLXX).

Here is information on the funds mentioned:

• Vanguard Treasury Money Market Fund (VUSXX)

https://investor.vanguard.com/investment-products/mutual-funds/profile/vusxx

• Fidelity ® Treasury Only Money Market Fund (FDLXX)

https://fundresearch.fidelity.com/mutual-funds/summary/31617H300

Tax Reporting and 1099 Issues

Holding the right fund is only half the job. The tax benefit still has to be reported correctly on the tax return. Just because a money market fund invests in Treasuries does not mean the 1099 will automatically show the state-exempt portion clearly.

Treasury-only money market fund income is often reported on Form 1099-DIV as ordinary dividends. The form may not clearly separate how much of the income is exempt from California state income tax. This is where mistakes can happen. Some tax preparers may enter the 1099 exactly as printed unless the client provides the fund company’s year-end tax document showing the government obligations percentage. Some preparers will make the manual adjustment when they have the supporting information. Others may not. That is why I prefer having a tax professional handle the reporting and giving them the supporting documents upfront. For example, if the fund is from Vanguard or Fidelity, I would provide the year-end government obligations percentage document along with the 1099. Then I would confirm that the California subtraction is properly reflected on Schedule CA.

This is also one reason direct Treasury bills can be simpler from a tax reporting standpoint. Treasury bill interest is generally reported on Form 1099-INT in a way that is easier for tax software and tax preparers to identify as state tax-exempt. Do not assume the tax benefit happens automatically. If the fund qualifies for a state income tax exclusion, make sure the documentation is provided and the adjustment is actually made on the tax return.

The right cash management option depends on what the money is for. Money needed for everyday spending belongs in a checking account. If we want simple savings with FDIC insurance, a high-yield savings account is usually enough. If the cash is already inside a brokerage account and we want a competitive yield, a money market fund can make sense. In a taxable account, especially for investors in states with income tax, Treasury-only money market funds and Treasury bills deserve a closer look because the after-tax yield may be better. If the money is needed on a specific date, Treasury bills or brokered CDs can help lock in the rate. For an emergency fund, the decision usually comes down to what matters most: insurance, convenience, liquidity, or after-tax yield. Municipal money market funds and MYGAs can also fit, but only after we compare taxes, liquidity, penalties, and the purpose of the money. Inside a retirement account, the tax-equivalent yield does not matter because the distributions are taxed based on the type of account. In a taxable account, the quoted yield is only the starting point. What matters most is what we keep after tax.

Please note that this material is for general educational and tax-planning purposes only. Tax laws are complex, there are exceptions to the rules, and the information may change over time. I do not provide tax and legal advice. Be sure to speak with a qualified tax professional about tax-exempt treatment, reporting requirements, and how to properly handle any state-exempt income. Thank you for watching. Until next time, this is Tan, your Trusted Advisor.